Savvly's Longevity Benefit is a S&P 500 ETF-based index fund with a Longevity Bonus. A transparent capital markets structure designed to potentially pay out more to those who stay longer.

No black boxes. No insurance company taking a cut. Every dollar is traceable through a straightforward capital markets structure.

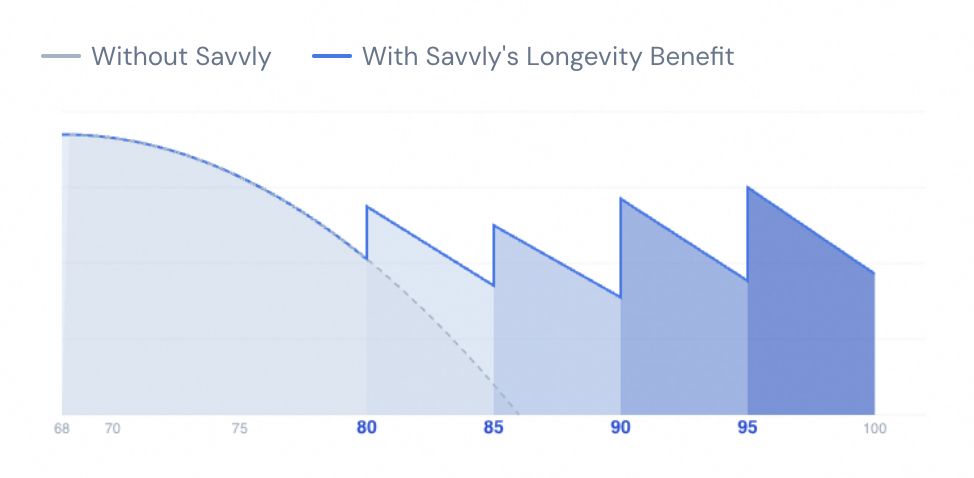

Savvly's Longevity Benefit distributes your accumulated balance as four potential cash payouts: at ages 80, 85, 90, and 95. These are designed to arrive at the moments when traditional retirement savings are most likely to thin out.

The payout structure is weighted toward earlier milestones: 40% of your potential benefit at age 80, 30% at age 85, 20% at age 90, and 10% at age 95, subject to fund terms, market performance, and investor outcomes.

Early exiters' unused capital may be reallocated to those who stay.

Hypothetical illustration only. Payout amounts are not guaranteed and depend on S&P 500 market performance, fund size and investor behavior, contribution amounts, timing, and other factors. The 40/30/20/10% payout schedule is subject to fund terms and investor outcomes. Past performance is not indicative of future results. Investment involves risk, including possible loss of principal. See full assumptions and disclosures at savvly.com/disclosures.

Hypothetical illustration only. Not a guarantee. Actual outcomes depend on S&P 500 performance, fund behavior, contribution amounts, and timing. Investment involves risk, including possible loss of principal.

Live in under a week. No discrimination testing. No health screening. Works alongside existing 401(k) plans without replacing them.

Add a longevity layer to client portfolios. Wealth transfer built in. No insurance license required.

Bring a genuinely new Longevity Benefit to your clients. Simple broker economics. First-mover advantage in an uncrowded category.

Book a 30-minute demo and we'll walk through the mechanics, the projections, and how Savvly fits into holistic plans.

Book a Demo