.png)

Become a founding investor and get lifetime benefits – plus a free look for two years.

Learn More

The Savvly Fund is designed to help provide more money when you need it most – in your later years. Invest a small portion of your savings today for the potential of bigger payouts the longer you live.

Plan your Savvly Retirement

.png)

.png)

We created Savvly because the current options weren't cutting it. The Savvly Smart Pension is efficiently designed to give you long-term financial security at a fraction of the cost of the alternatives.

.svg)

.svg)

.png)

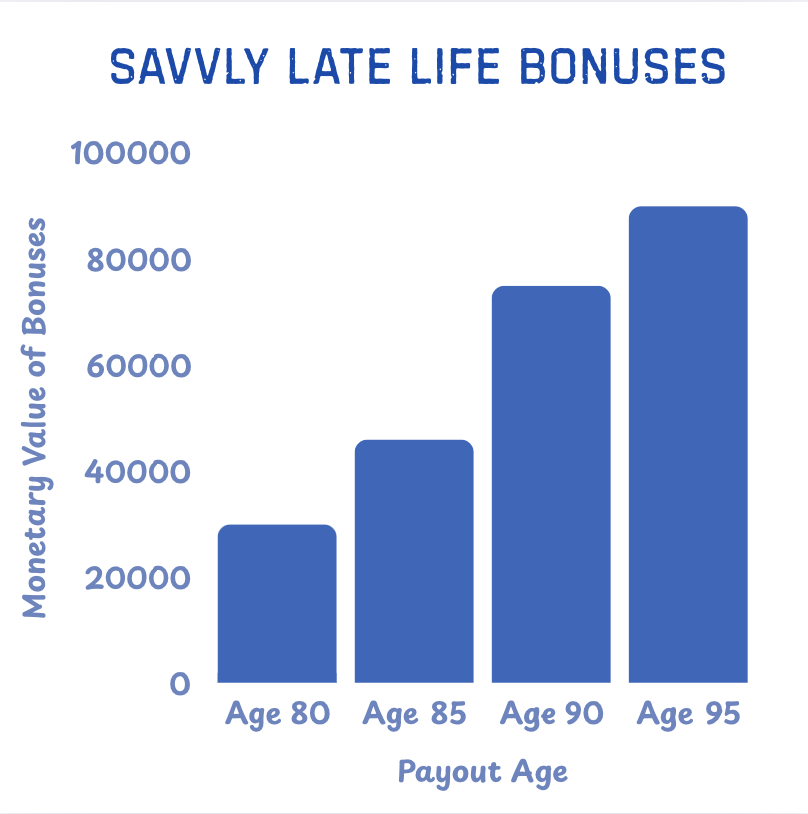

Savvly is a modern personal pension solution designed to help you secure your retirement. The pension portfolio consists of low-cost index funds from leading asset managers like Vanguard, along with up to 10% invested in the Savvly Fund. The Savvly Fund pools investments among participants, allowing those who stay in the fund long-term to benefit the most. By investing a portion of your savings in the Savvly Fund, you receive long-life bonuses that help maximize your paychecks, ensuring peace of mind in retirement.

No, the Savvly Fund is not an insurance policy or annuity. There’s no insurance company taking profits. Instead, all contributions stay within the Savvly Fund, and those who remain invested long-term benefit more from the investment pool.

No, the Savvly Fund is not a typical investment fund. Your assets are invested in a low-cost S&P 500 ETF, managed by a third-party custodian (Apex Group), ensuring secure, long-term growth. Savvly manages the process of new investors entering an existing pool.

The Savvly Pension is structured as a personal retirement account that includes the Savvly Fund. The Savvly Fund enables a minimum level of pooling among the independent personal retirement accounts. The Savvly Fund helps investors provide stable, lifelong income that can grow as people age.

Savvly is open to anyone. The minimum investment starts at $100/month, and there is no long-term commitment.

We recommend contributing as much as you feel comfortable investing in your retirement. When the Savvly Pension is used in a qualified account (IRA o ROTH IRA), the Federal Government does not allow penalty-free withdrawals before 59 ½. If you want full unrestricted access to your fund, you should consider opening the Savvly Pension in our standard brokerage account.

Good news. The Savvly Pension can sit on both non-qualified brokerage accounts or a qualified account like IRA and ROTH IRA.. This means you can use funds from your savings, brokerage, or checking accounts— and Savvly accepts IRA rollovers.

If you withdraw or pass away, you or your estate will receive the net asset value (NAV) of the investment in your account: bonds, equity, and the Savvly Fund. The value of the Savvly Fund, which typically weighs less than 10% of your account, depends on your age and the performance of the S&P 500. Generally, the value of the Savvly Fund is at least 75% of the investment amount and can be up to a multiple of the performance of the S&P 500 during your investment period, depending on the age of withdrawal. See details here

The IRS may impose penalties for early withdrawals in qualified accounts.

You can choose to begin receiving monthly paychecks anytime, with no upper age limit. Payouts are based on a target 100-year lifespan and may change based on inflation and market returns, ensuring you always have recurrent income, no matter how long you live. You can withdraw all your assets anytime if you wish.

Your investment is securely held in a standard brokerage or qualified account. Your assets remain in your name all the time and are never on Savvly’s balance sheet. The funds are held by a third-party custodian (Apex) to ensure safety and transparency.

No medical exam or health history is required. Your Savvly Pension is based purely on financial contributions and doesn’t take your health into account. However, Savvly is designed for those who expect a long retirement, beyond 80 and want to prepare accordingly starting early in life.

It depends on the type of accounts you choose when you sign up. Taxation is deferred for qualified accounts like IRA and ROTH IRA. Savvly does not provide tax advice.

.svg)

.svg)

.svg)

.svg)